By David Sierra, Head of European Products at Energy One

Europe’s energy markets are no strangers to volatility. However, with current conditions placing them under intense pressure and price fluctuations reaching historically high levels (that appear likely to persist), it is time to rethink the approach.

Rather than treating volatility as a hostile threat and a risk to be avoided at all costs, it should be seen as a structural feature of today’s markets; one that must be understood, managed and ultimately leveraged to create new forms of value.

That was the point I explored at the European Industrial Energy Days expo and conference last month. In my presentation at the event, the mission was simple: I wanted to share how businesses can manage energy risk and operations through smart technology, deep market expertise and flexible solutions.

This article distils the key messages from that presentation into a practical narrative for industrial players and energy-intensive businesses navigating today’s turbulent markets.

Let’s start with the killer question: Why is energy price volatility so extreme?

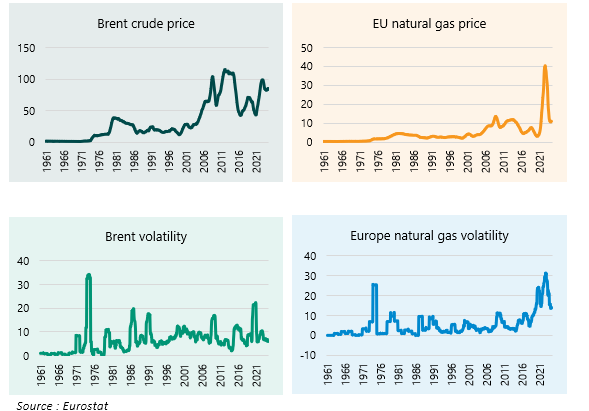

Energy price volatility in Europe is no longer episodic; it’s structural. Multiple forces are interacting across different time horizons, amplifying uncertainty.

Over the long term, volatility is shaped by several drivers, including:

- Regulatory and geopolitical risk

- Fuel and carbon pricing mechanisms

- Supply and demand balance

In particular, with the gradual move away from long term supply contracts in favour of wholesale markets, combined with the rapid growth of LNG, long term gas and power markets have become more exposed than ever to global events. This sensitivity has been clearly illustrated by the conflict between Russia and Ukraine and, more recently, by the closure of the Strait of Hormuz.

In the short term, the effect is even more visible, and markets react violently to drivers such as:

- Weather-driven renewable variability

- Grid constraints and outages

- Solar penetration

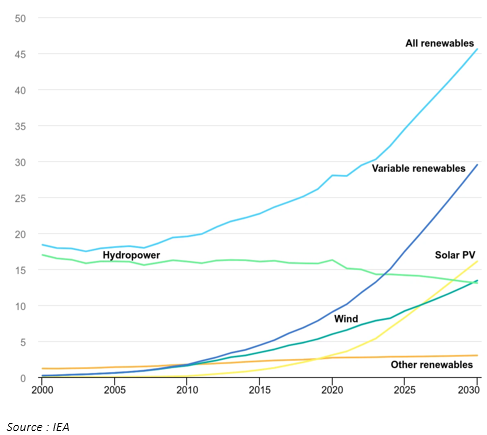

Renewables have recently become the leading source of electricity generation in Europe. In the past, gas or other thermal plants typically set the marginal price during most part of the day. Now, it is more often renewables that define this price, especially around midday and during the summer, leading to much sharper price swings.

One direct consequence is the explosion in negative price hours, which were almost non-existent before, and more broadly, the significant price distortions within a single day. This is the now well-known Duck Curve in intraday prices, and it continues to deepen.

Volatility is here to stay

Here is the truth no one likes to hear: volatility is not going away.

If we take a step back, one thing becomes clear: geopolitics and renewables are now the two primary forces shaping energy markets, and neither of them are about to fade away.

On the geopolitical side, recent developments, once again, show that we are not heading toward de-escalation or simplification. Quite the opposite. The environment remains marked by recurring tensions and long-term uncertainty. At the same time, renewables are still far from reaching a maturity phase, installed capacity keeps growing and its impact on price formation is set to intensify, particularly over the coming months, bringing stronger intraday swings and an increasing frequency of negative price hours.

Volatility, in other words, is no longer an occasional phenomenon; it is becoming a structural feature of the market. And this leads to a simple but fundamental conclusion: the days of passively absorbing volatility are behind us. The real challenge now is to put in place strategies that actively manage it, because in today’s markets, volatility will either remain a cost, or become an opportunity.

The hidden cost of “doing nothing”

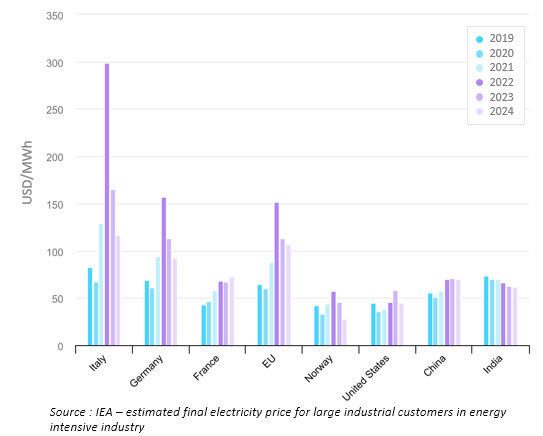

For industrial and commercial energy users, volatility has a direct and often underestimated impact on profitability: same consumption, very different cost.

Fixed contracts embed risk premiums, meaning companies often overpay during calm markets, whilst flexible contracts expose businesses to price spikes without capturing value when prices collapse. Without a strategy, many organisations end up paying twice – once for protection, once for exposure – and never get rewarded.

This dynamic is particularly damaging for energy intensive industries, where rising and unpredictable energy costs erode margins and delay critical investments.

Turning volatility into opportunity

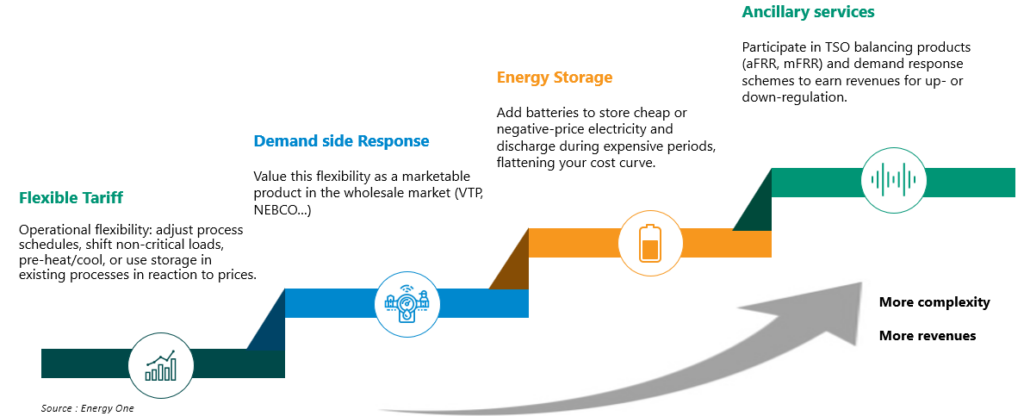

Leading organisations are shifting from defensive energy strategies to proactive ones. The goal is not just to reduce risk, but to monetise flexibility.

We believe value can be created in many ways:

- Bring renewables closer to consumption: onsite or local renewable generation reduces exposure to wholesale price swings while creating optionality

- Use flexibility to shift energy in time – buy low, use high: energy storage and flexible loads allow companies to buy electricity when it’s cheap (or even negatively priced) and use it when prices are high

- Procure intelligently: Modern strategies include:

- Power purchase agreements (PPAs) – to secure long-term supply

- Flexible tariffs – to monetise flexibility

- Hybrid fixed‑flex structures

- In‑house balancing responsibility (BRP) – to take full control of procurement and market exposure

- Digitise energy management: real‑time data, forecasting and automation turn complexity into control

- Access flexibility markets:demand response, ancillary services and balancing markets allow industrial assets to earn revenue from their flexibility, turning operations into market participation

From scary markets to simple playbooks

At first glance, setting up these processes and participating in new markets can feel intimidating, whether because of IT impacts, new data requirements or the administrative work involved in obtaining additional licences. This perception is understandable, as the complexity can seem significant when viewed as a whole.

The good news, however, is that you do not have to navigate this transition on your own. With the right partners and the right technology, managing this complexity becomes far more accessible, turning what initially looks like a constraint into a genuine plug and play opportunity.

To speak to our experts about how you could turn volatility into value, submit your details via our Contact Form.